Now Reading: Mizuho Slashes Alexandria Target by $30—Shocking Drop Ahead

-

01

Mizuho Slashes Alexandria Target by $30—Shocking Drop Ahead

Mizuho Slashes Alexandria Target by $30—Shocking Drop Ahead

Table of Contents

Mizuho Adjusts Price Target on Alexandria Real Estate Equities in a move that has caught the attention of investors, financial analysts, and stakeholders in the real estate investment trust (REIT) market. The Japanese investment bank revised its target price for Alexandria Real Estate Equities, Inc. (ARE) to $91, down sharply from the previous $121 estimate. This $30 reduction signals a significant reassessment of the company’s near-term prospects and market position.

Why Did Mizuho Cut the Price Target?

The price cut by Mizuho comes amidst a broader environment of uncertainty surrounding commercial real estate, particularly life science campuses, in which Alexandria specializes. Rising interest rates, weaker leasing volumes, and increased scrutiny over real estate portfolios have all contributed to this revision.

Mizuho cited continued softness in tenant demand, delayed construction timelines, and persistent valuation pressure in the real estate sector as core reasons for their downgrade. Analysts at Mizuho are also concerned about Alexandria’s return on invested capital (ROIC), which has reportedly lagged in recent quarters compared to expectations.

This downgrade reflects broader caution in the REIT sector, especially in specialized office spaces that have not fully recovered from post-pandemic shifts in work and research behavior.

Impact on Investors and Market Sentiment

The announcement from Mizuho immediately impacted market sentiment. While Alexandria’s stock has experienced a slow recovery in early 2025, the sudden and steep price target revision has shaken investor confidence. The stock was already trading well below its 2022 highs, and this latest change may further discourage institutional investors from increasing exposure in the near term.

Retail investors may also interpret the downgrade as a red flag for the company’s long-term growth trajectory. The reaction in pre-market and early trading sessions following the report reflected this unease, with ARE shares dipping slightly in response.

What Is Alexandria Real Estate Equities?

Alexandria Real Estate Equities is one of the largest publicly traded real estate investment trusts in the U.S., specializing in life sciences and technology campuses located in top innovation clusters such as Boston, San Francisco, and San Diego. It owns and operates high-quality lab and office properties used primarily by biotech firms, pharmaceutical companies, and scientific research institutions.

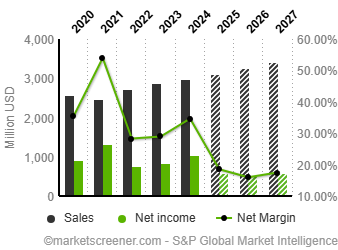

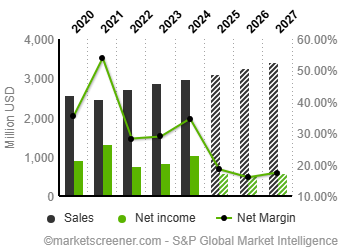

The REIT model adopted by Alexandria focuses heavily on long-term leasing with industry-leading clients, including major pharmaceutical companies and research universities. As of 2025, the company owns over 74 million square feet of rentable space.

However, the niche focus also exposes the company to sector-specific risks, such as the downturn in biotech funding and R&D expenditure, which has been slowing due to economic conditions and funding cutbacks.

How This Downgrade Aligns with Broader Market Trends

Mizuho’s adjustment reflects a larger trend: REITs are being reevaluated as interest rates stay high and macroeconomic indicators remain mixed. Across the real estate landscape, investors are demanding higher yields and faster execution of development pipelines, both of which are currently under pressure for Alexandria.

Several other firms have also trimmed their outlook on the REIT sector, citing the need for more adaptive real estate strategies. Alexandria’s business model, while robust in the pre-pandemic era, may require modification to align with hybrid work models and slow-paced tenant expansion in research-driven industries.

What This Means for the REIT Industry

The Mizuho Adjusts Price Target on Alexandria Real Estate Equities not only signals issues for one company but also raises questions about the future of specialized REITs. If an industry leader like Alexandria is facing significant valuation cuts, smaller or less diversified REITs could be at even greater risk.

Moreover, investors are increasingly shifting focus toward REITs that generate high immediate income rather than relying solely on long-term growth narratives. This places pressure on Alexandria to rethink capital deployment and enhance its dividend sustainability amid challenging conditions.

Company Response and Future Outlook

Alexandria has not issued a formal statement in response to Mizuho’s downgrade as of this writing. However, during its last earnings call, the company emphasized its strong tenant retention, a robust development pipeline, and a conservative balance sheet as key strengths.

Despite the price target cut, Mizuho has not changed its rating on the stock, which remains at “Neutral.” This suggests that while there are near-term challenges, the long-term fundamentals of the company are still relatively stable, provided it adapts to shifting market dynamics.

Alexandria’s next quarterly earnings report will be crucial in providing more clarity on the company’s direction. Investors will closely watch metrics such as occupancy rates, net operating income (NOI), and capital recycling strategy.

Should Investors Be Worried?

The short answer: It depends on your investment horizon. For short-term traders, the downgrade is undoubtedly negative, as it will likely create price volatility and discourage bullish sentiment. For long-term investors, however, Alexandria still offers a unique market position in a specialized sector with high barriers to entry.

Still, the Mizuho price adjustment is a wake-up call. It tells the market that even top-tier REITs are not immune to changing economic landscapes and investor expectations. Investors should revisit their portfolio allocations and consider the broader implications of sector-specific risks in REIT investments.

Conclusion

The move by Mizuho to adjust its price target on Alexandria Real Estate Equities to $91 from $121 serves as a strong reminder of the dynamic nature of real estate investing. As the REIT sector navigates through economic headwinds, shifts in work models, and changing investor priorities, even the most respected players must adapt quickly.

For now, all eyes are on Alexandria’s response and performance in the upcoming quarters. Whether this price cut turns out to be a temporary correction or the beginning of a long-term reassessment depends entirely on how the company manages its portfolio, tenant relationships, and strategic investments going forward.

Also read – Home Inspection: ₹4.3 Cr Bandra Deal Shocks Bollywood